With the open enrollment period for purchasing individual health insurance on the federal and state exchanges starting on November 1, I’m doing a series of posts to make it easier for freelancers to make informed choices about their healthcare. Stay tuned for more installments throughout the month of October.

Other installments:

- Why freelancers should keep their health insurance in 2019

- What type of health insurance plan is best for freelancers?

When we talk about the cost of health insurance, what we’re normally referring to is the premium: the amount that we pay every month to own an insurance policy. Because of the regularity of this expense it is the one that people focus on the most when choosing a health insurance plan. But there are other costs involved with health insurance, and picking a plan solely because it has the lowest premium may wind up costing you more in the end.

The non-premium costs associated with health insurance are known as out-of-pocket costs (though your insurance company may use the friendlier term “cost sharing”). In general, the lower your premiums are, the higher your potential out-of-pocket costs can be. I say “potential” because out-of-pocket costs aren’t fixed: they depend on how much and what kind of healthcare you need. Plans with lower premiums leave the patient responsible for a higher percentage of their healthcare costs than higher-premium plans, so if you need major or frequent medical care your higher out-of-pocket costs may offset the cheaper premiums that you pay.

Let’s look at the most common types of out-of-pocket costs. Keeping all of the terminology straight is hard if you have no experience with health insurance, but I find that it’s helpful to think of three different layers of costs:

- Layer 1 is your co-payment, a fixed fee that you pay every time you receive a certain service like a specialist visit or prescription drugs. Co-payments can range from ten to a hundred dollars or more depending on the service, so if you are frequently receiving certain types of healthcare it’s important to know your co-payment for those services.

- Layer 2 is the plan’s deductible: the amount that you pay out-of-pocket each year for all healthcare before the plan starts to pay anything. Though rising premiums have gotten the most attention in recent years, insurance companies have also been increasing the deductibles in their plans, giving patients a higher cost hurdle to attain before they see any benefits.

- Layer 3 can be a surprise for many people who aren’t experts on health insurance. Even after reaching their plan’s deductible, patients may still be responsible for paying part of their plan’s costs above that amount. This is called co-insurance. An insurance policy may specify a 20% co-insurance above the deductible. This means that after paying for 100% of their costs up to the deductible, the patient will pay 20% of the remainder.

ACA plans are divided into tiers – bronze, silver, gold, and platinum – and the higher the tier, the lower your out-of-pocket expenses will be in general. All ACA-compliant plans have a cap on total out-of-pocket expenses, and again the higher the tier, the lower that cap will be. Out-of-pocket caps usually don’t include premium payments or any non-emergency care received outside of the insurance plan’s network.

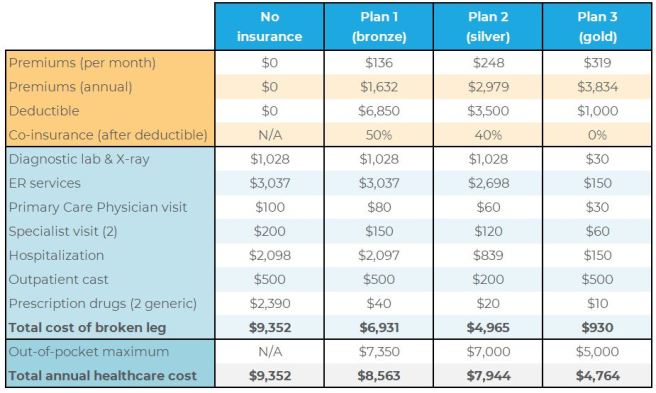

People who are generally healthy may be able to get away with a policy with a low-premium plan if they can somehow avoid any medical mishaps during the year. But health can be hard to predict: accidents happen, and unexpected illnesses that turn into hospital stays can rack up huge medical bills. An “inexpensive” plan can quickly become just the opposite with one surprise medical event. The below is a hypothetical comparison of the out-of-pocket costs for a broken leg with three of the individual plans available this year through the national ACA exchange in my home state of Nebraska. The premium costs are based on a single 33-year-old male making $40,000 per year.

Despite having a monthly premium $183 higher than than the bronze plan, the gold plan covers $6,000 more in medical costs, easily surpassing the difference in premium. This is just one of many potential scenarios for how healthcare coverage can pan out, but it shows how focusing on premiums alone can become an expensive choice with just one unexpected event.

As a freelancer, getting sick may also leave you unable to work and, unless you have disability insurance, you could be incurring these costs at a time when you don’t have any income. This double-whammy of bad luck can be financially ruinous to a freelancer who doesn’t have the funds saved to cover their costs of living or healthcare.

It’s important to estimate your healthcare needs and consider the possibilities of an unforeseen event before choosing a health insurance plan. Picking a plan solely on the basis of a lower premium cost may ease the stress on your monthly budget, but it can leave you at risk of a large, unpredictable medical expense. I’m not saying that everyone needs to pay for a gold or platinum plan that covers everything under the sun, but if you opt for a lower-tier plan, you should also have a plan to cover your out-of pocket costs when they arise.