With the open enrollment period for purchasing individual health insurance on the federal and state exchanges starting on November 1, I’m doing a series of posts to make it easier for freelancers to make informed choices about their healthcare. Stay tuned for more installments throughout the month of October.

Other installments:

- The cost of healthcare: It’s not all about the premium

- What type of health insurance is best for freelancers?

From 2009 until 2011, in the bad old days before Obamacare, I had no health insurance. It was a reckless gamble on my own health, but at that time, freelancers without a day job or a spouse with an employer plan were forced to make a distressing choice: pay for expensive, often-shoddy individual insurance, or go without and risk being unable to afford the costs of an unexpected medical event.

It’s easy to complain about the healthcare industry today – and the system as it is is far from perfect – but it’s worth remembering just how bad things had gotten before the Affordable Care Act was enacted in 2010. Health insurance claims were routinely denied because of pre-existing conditions. Plan benefits were often capped and patients with severe health issues would have funding for their care cut off mid-treatment. Coverage for routine or preventative care was inconsistent, the details often buried in fine print.

Obamacare ended these practices and set minimum standards of healthcare coverage that all insurers must follow, both for individual plans and for those provided by employers. It made real healthcare coverage – not the haunted-house plans, full of trapdoors and unseen horrors, that existed during my freelancing years – available to people without access to an employer plan, and made those plans more affordable through tax credits and subsidies that reduced monthly premiums. The Affordable Care Act was a game-changer for freelancers.

Back in 2009, my decision to gamble on my health was only partially a calculated one. On a struggling musician’s income I couldn’t have afforded the premiums for the plans available at the time anyway, and doing some research into the coverage they offered gave me little confidence that they would be of much help if I got sick. But I also reasoned that a guy in his mid-twenties with no chronic ailments who kept himself in decent shape had no reason for healthcare, and the premiums I would be paying into a system I didn’t use would be money down the drain.

Of course, that’s exactly how insurance is supposed to work. Many people pay into a system they don’t use on the off chance that they’ll need it someday. If people only buy insurance when they’re certain to need it – before having a baby, for example, or even after they’ve already gotten sick – the system can’t support itself. So my privileged choice to forego insurance deprived the system of one healthy, premium-paying person, and made the whole thing a tiny bit more expensive for everyone involved. Except me.

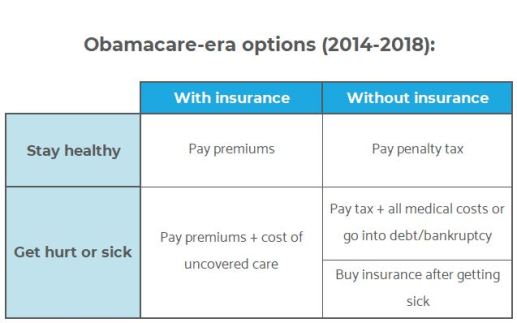

That’s why the Affordable Care Act instituted a penalty tax on people not covered by a qualifying health insurance plan. The individual mandate forced most people to pay into the system, either through insurance premiums or the annual penalty, to ensure it wouldn’t collapse on itself. Some still opted to go without insurance and pay the penalty, but most people, given the choice between paying the tax and getting nothing in return versus buying insurance and its guaranteed benefits, chose the latter option.

The law’s ban on insurers denying claims for pre-existing conditions introduced another option: you could simply wait until you get sick to sign up for insurance and enjoy its benefits. This is truly the gambler’s approach, because other than Special Enrollment Periods you can only enroll in an Obamacare plan that starts on January 1 of the following year. Waiting until you get sick to buy insurance assumes you won’t be too sick to wait a little while longer until the plan kicks in.

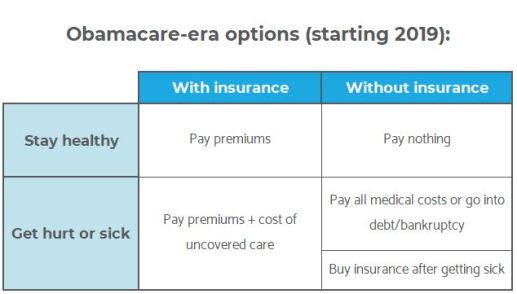

The tax law that the Republicans passed in 2017 gives freelancers the incentive again to gamble on their own health. Beginning in 2019 there will be no penalty tax for opting out of health insurance, which for the reasons above is already resulting in increasing premiums for those remaining in the system.

As this year’s Open Enrollment season approaches, many freelancers are going to be asking whether it makes sense to keep their current insurance or to drop it and hope for the best. As housing and other costs continue to rise, it can be hard to stomach another rate increase on your health insurance premiums. If you’re young and healthy shouldn’t you just save your money until you’re older and more likely to have health problems?

The table above shows the outcomes you are selecting by choosing to go either with or without health insurance. For some people who are having planned surgery or who have conditions requiring prescription drugs, the decision is obvious: insurance is just part of the cost of living a normal life. If you’re currently healthy enough to avoid seeing a doctor more than once a year, your outcome depends entirely on whether or not you have an unexpected illness or accident.

If you’ve never had an unlucky break or an accident like I did a few years ago, chances are you’re more willing to risk it. If you have, you’re probably thinking harder about insurance. We tend to downplay the odds of things that haven’t happened to us personally and to overemphasize those that have, when in reality the risks for all of us who leave our homes every day to go do everyday things are roughly the same.

So how much are you willing to bet on staying healthy for the next year? The total cost before insurance of my own accident – which required an ambulance trip, an ER visit, and a year of chiropractor visits – ran well over $10,000, and that was for a relatively minor accident. The effects of a serious medical event will leave an uninsured person financially wiped out for years, either through medical debt or bankruptcy. The reality is that health care in America today is expensive, and paying for health insurance and saving for out-of-pocket costs (either in a health savings account or a dedicated emergency savings account) should be a part of your budget.